Equities: Unfazed by phases

WestEnd Advisors Investment Team 18-Jan-2023

Astronomy buffs and moon-watchers are not the only ones who should be keen on phases. Investors might be wise to pay close attention to the various phases of our economic cycle before making equity allocation decisions. In fact, we believe that dynamic sector allocation—and avoidance—based on the economic cycle can be a basis for generating excess return over time and irrespective of market backdrop.

One key point worthy of repeating is the idea of what you don’t include in a portfolio can be as important as what you do. A deeper understanding of the economic cycle and how certain sectors have tended to respond based on the underlying macro picture can provide useful guardrails for portfolio construction. In other words, we believe looking at past patterns of relative sector performance that have tended to play out over various phases of the economic cycle provides an effective, forward-looking foundation for building a more durable portfolio.

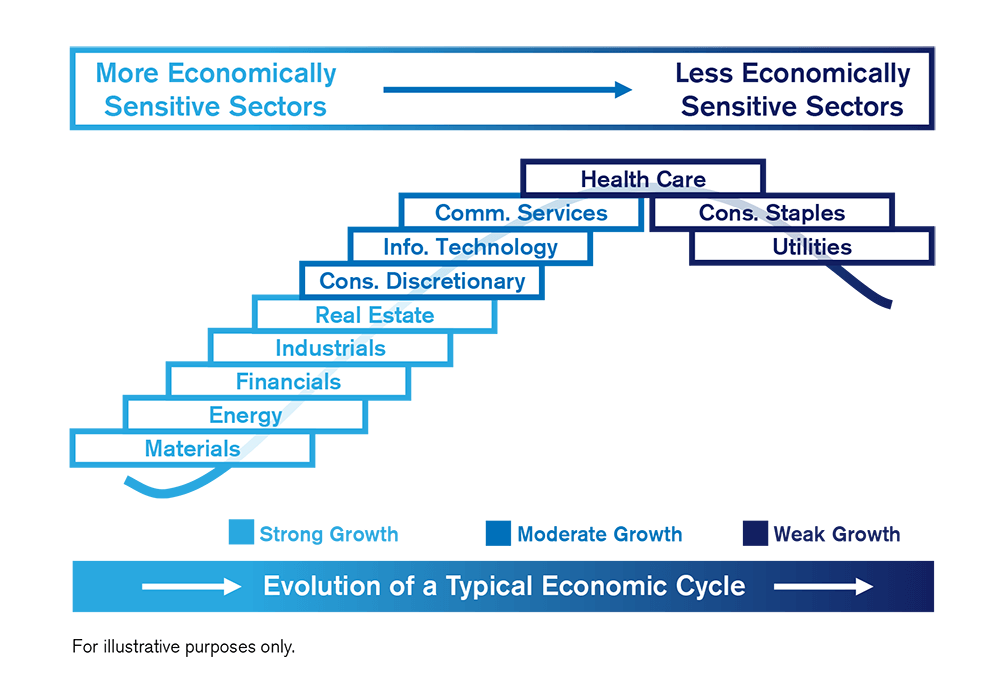

Focus on Phases

Our experience has taught us that the revenue and earnings variability of companies in what we consider early-phase sectors, those with some of the highest economic sensitivity, is typically much greater than those in late-phase, more defensive sectors. For example, we’ve historically seen Oil & Gas industry revenue growth be significantly more volatile than Health Care Providers’ industry revenue growth. In that sense, we believe the Materials, Energy and Financials sectors—among others—are typically poised for outperformance in the early parts of the economic cycle, when the economy has tended to rebound sharply. But when the cycle starts to age and economic growth moderates, the downside of that revenue volatility can also set the stage for potential underperformance.

What does this mean for portfolio positioning as we look out toward 2023? Consider Energy, for example, an early-phase sector in our view. Energy has outperformed sharply in 2022. In hindsight, that’s not very surprising given the inflationary environment and the boost to oil prices tied to Russia’s invasion of Ukraine. However, we have not embraced the U.S. Energy sector in portfolios at this late stage of the cycle, as the prospect of slower growth in the U.S. and abroad increases the likelihood of a deterioration in the earnings outlook for the sector. This is just one example of sector-avoidance we typically pursue in the later stages of an economic cycle, which is where we believe we are today.

By contrast, mid-phase sectors—such as Information Technology, Consumer Discretionary and Communication Services—have tended to have less cyclical revenue exposure than early-phase sectors, but more sensitivity to economic growth than late-phase sectors. Thus, we continue to see the lower revenue volatility and more secular-oriented growth profiles for these mid-phase sectors as an attractive way to maintain some economic sensitivity in portfolios at this stage in the cycle. Businesses and consumers have increasingly embraced digital platforms in recent years, and business investment spending on information processing equipment and software rose to an all-time high last year. Looking ahead, even as economic growth slows, we expect businesses will continue to invest in technology to increase productivity in a slower-growth environment, particularly given tightness in the labor market and labor cost pressures.

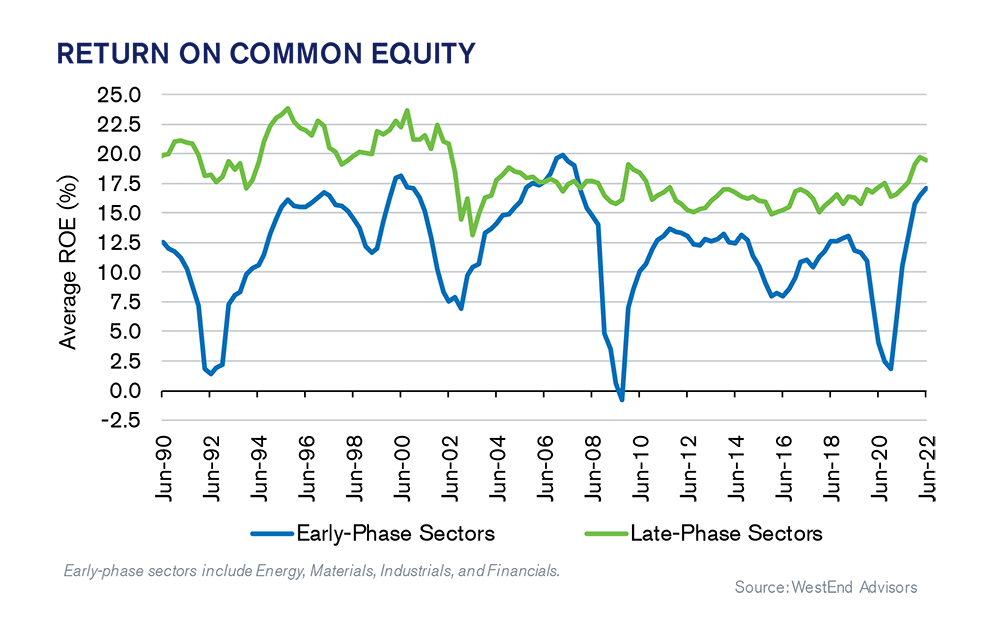

We increasingly see the financial stability of late-phase sectors—Health Care, Consumer Staples, and Utilities—as desirable as the economic cycle matures and the risk of a slowdown in growth increases. Defensive, late-phase sectors have generated above-market return on equity (ROE) over time, and their ROEs have typically been very consistent. Alternatively, economically sensitive sectors like the early-phase Materials, Industrials, and Financials sectors have shown much more cyclical ROEs, as illustrated in the chart below that looks back over several decades.

Simply put, we believe exposure to these traditional defensive areas of the market is warranted today, especially relative to economically sensitive areas of the market, in our view.

These are just a few examples that illustrate how sector performance can be linked to different economic phases, and how this philosophy can be used to tilt portfolios in ways that may better align with the macroeconomic and market environments.