Fixed Income: Weathering the storm

Joseph Morgart 18-Nov-2025

As we head into year-end and look out to 2026, investors may be inclined to revisit their income-oriented portfolios in an effort to add more yield potential, broader diversification, or both. After all, the Federal Reserve has begun a new rate-cut cycle, and yields have been heading lower across the Treasury curve. With that in mind, where might investors look?

One alternative to traditional and more well-known fixed income investments is catastrophe (cat) bonds. This sector offers potentially attractive risk-adjusted returns and added diversification benefits. In fact, an allocation to this specialized sector could make bond portfolios more resilient, in our opinion, because the sources of risk, return, and liquidity are structurally uncorrelated with other asset classes.

A Quick Primer

Simply put, cat bonds are high-yield debt instruments and a means for investors to participate in the reinsurance industry, which has existed for more than 150 years. These bonds help insurers transfer the risk of major natural disasters, such as hurricanes, wildfires or major earthquakes, in return for higher yields. Importantly, investors can lose principal if a predetermined catastrophic event—often called a triggering event—occurs during the bond's risk term (typically one year, though sometimes longer).

However, you might be surprised to learn how infrequently investors have actually incurred principal losses. Over the past 17 years, one of the industry’s widely followed benchmark (the Swiss Re Global Cat Bond Index) has delivered positive performance in 16 of those years. This dynamic of positive returns is largely due to the industry’s demonstrated ability to reprice risk efficiently (i.e., raise premiums), after a catastrophic event. As a result, patient investors who tend to remain invested, rather than attempting to time entries and exits in this market, are often able to recoup quickly from potential drawdowns.

Broad Participation & Liquidity

Cat bonds were first introduced into capital markets in the aftermath of Hurricane Andrew in 1992, which caused enormous insured losses and challenged the solvency of several insurance companies. In response, the insurance industry created cat bonds to help protect against the unpredictable nature of natural disasters. Over the years, the cat bond market has matured greatly and now includes broad institutional investor participation, and it is expected to surpass $20 billion in new issuances for the calendar year 2025, according to projections from Moody’s. Clearly, the scale of this market illustrates that the cat bond market has found the proper balance as an effective risk-transfer mechanism for insurers on one hand, and a means for investors to capture attractive risk-adjusted returns on the other.

Today, there’s even daily liquidity for this segment of the bond market, though we believe it’s best used as a strategic allocation. We certainly do not advocate investors tracking NOAA weather reports as a basis for trading in and out of cat bond positions.

Uncorrelated Returns

We believe cat bonds may be able to play an important role in investors’ income-generating strategies. Attractive yields would be one obvious draw. But because cat bond performance is dependent on climate-related events, they do not move in lockstep with any traditional financial markets. Geopolitics, trade disputes, tariffs, monetary and fiscal policies, and investor sentiment do not materially impact cat bond performance. There is virtually no correlation between these assets and other segments of a traditional investment portfolio, and it remains a key reason for their continuing growth and popularity.

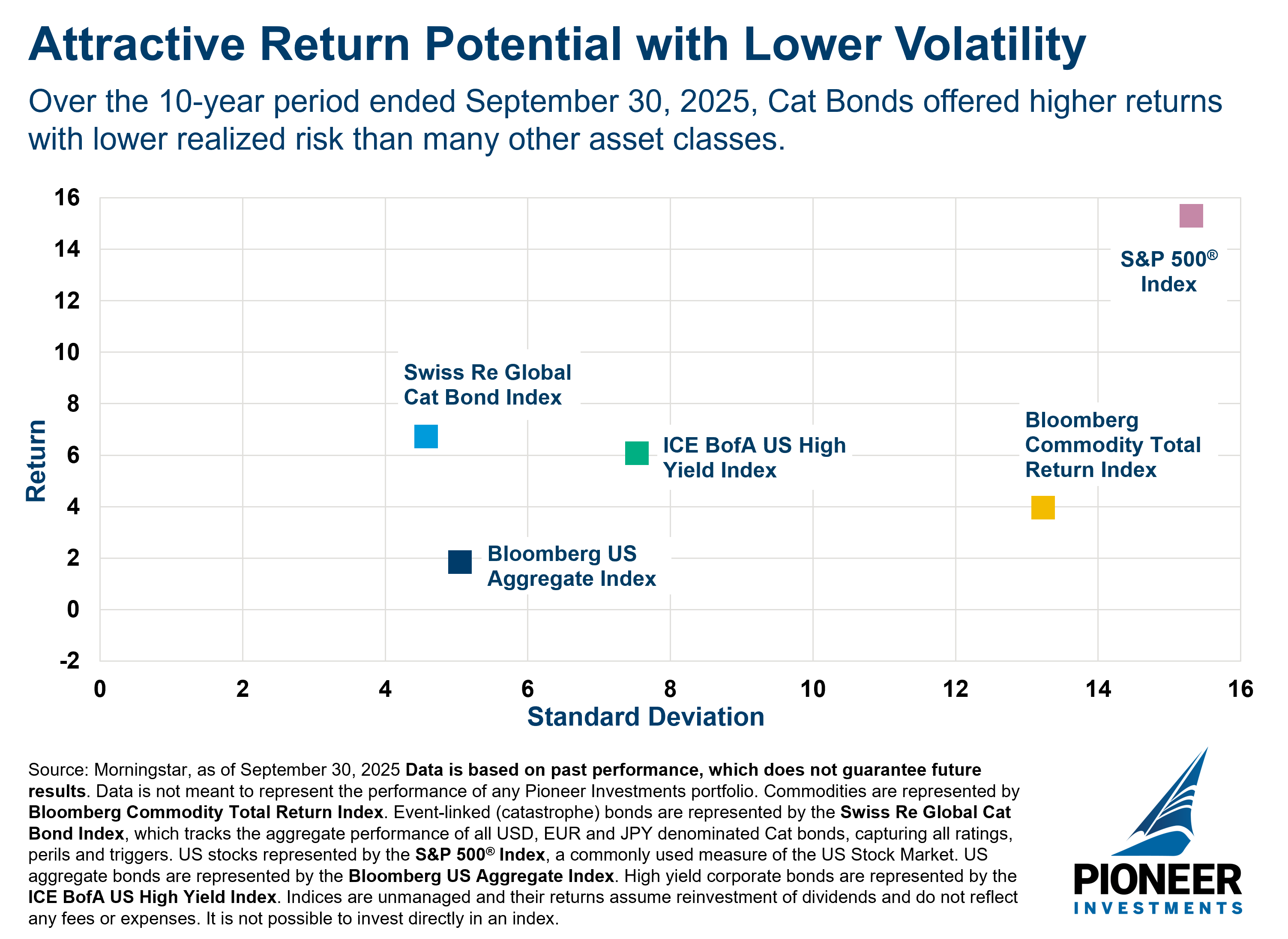

Furthermore, an actively managed cat bond portfolio should be able to manage risks by focusing on different countries/regions and perils, thereby achieving a further diversifying effect. Portfolio managers can also seek to mitigate risk by allocating to issuers who have demonstrated an ability to collect greater premiums or otherwise improve operations and profitability. Over the past decade, cat bonds, as represented by the Swiss Re Global Cat Bond Index, have offered more attractive risk/return characteristics than many traditional asset classes.

Exploring the Potential

From an asset allocation perspective, we believe adding some exposure to cat bonds is likely to improve the return potential of a bond or alternatives portfolio in a risk-savvy manner, while also enhancing its diversification features. There may be some risk of principal loss, as with virtually any investment, but we believe that the long-term performance of the reinsurance industry, as well as the evolution and growth of this fixed income sector, should give investors confidence. Importantly, for investors to receive the full potential benefits of cat bonds, we believe they should remain invested over the long term.