Fixed Income: The next chapter

Allyson Krautheim 23-Jan-2025

Change is in the air. It’s a brand-new year, replete with new political leadership now that a single party has gained control of both Houses of Congress, as well as the Executive Branch, for the first time in a long while. On top of that, the Federal Reserve is well into a new rate-cutting cycle, though uncertainties remain about how deep and how long the rate cuts will continue. All this is creating questions for investors who want to know how to position in this new environment. Will bonds continue to act as a ballast for equity portfolios? Are there opportunities to add incremental yield in a risk-savvy manner? And, if yes, how might that be best accomplished?

The Victory Income Investors team continually monitors the markets and offers a few thoughts on the current state of fixed income.

Still Your Portfolio’s Ballast

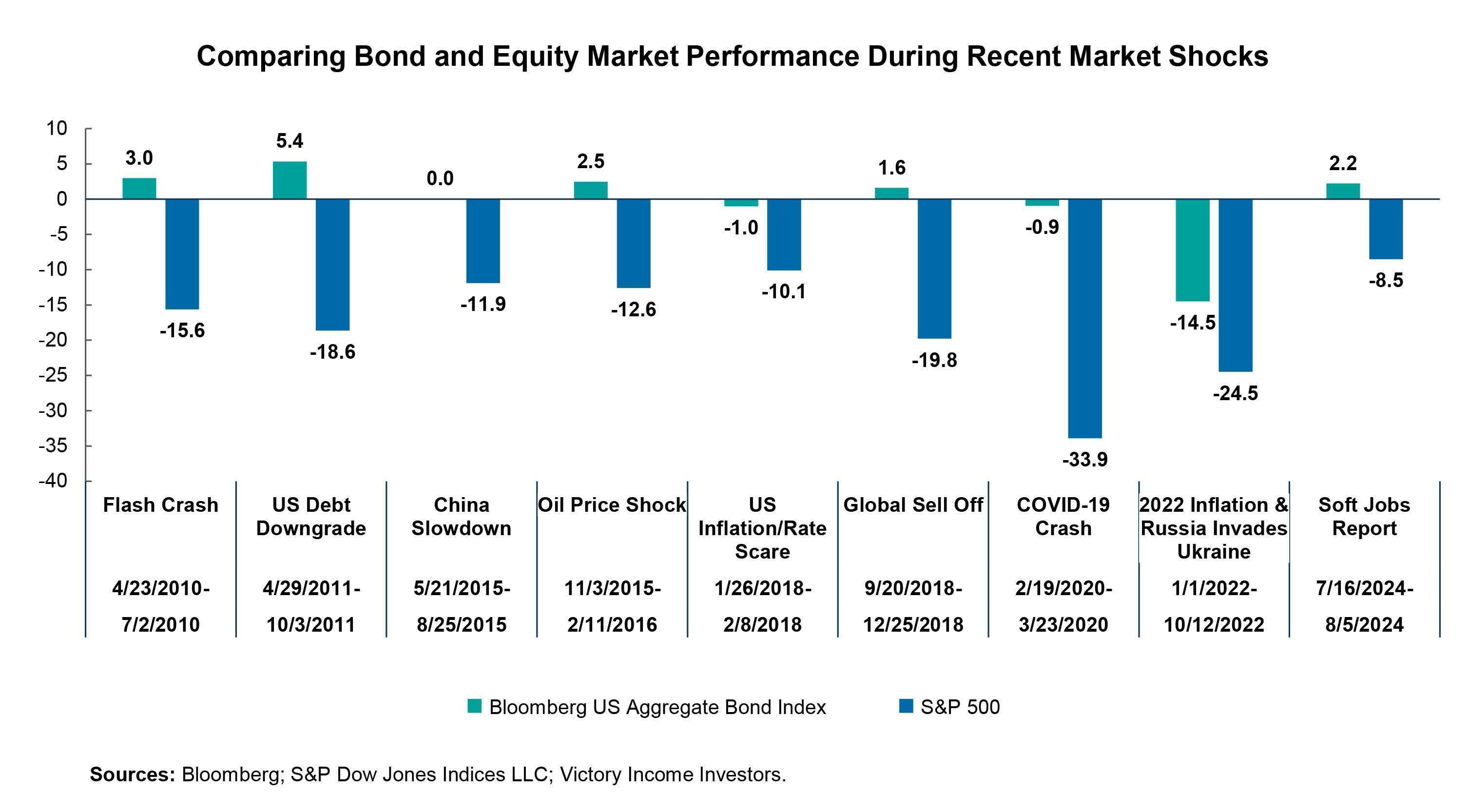

At a time when the S&P® 500 is putting up back-to-back years of impressive returns of 25% or more, it’s easy for bonds to become an afterthought. But having studied fixed income over the long term, we can say with confidence that bonds can be a ballast for your portfolio. It’s not that bonds are always negatively correlated to equities. However, bonds do tend to show their mettle during periods of equity market tumult.

The graph below compares the performance of equities (represented by the S&P 500) to a diversified bond portfolio (represented by the Bloomberg US Aggregate Bond Index) during periods of recent market turmoil. Even in 2022 when bonds declined steeply, the losses paled by comparison to stocks. And in many of these volatile periods illustrated below, bonds actually registered gains. This track record gives us confidence that bonds can still be your portfolio’s ballast in 2025 and beyond.

Get in the Game!

Victory Income Investors also believe that bonds remain relatively well positioned for 2025 on a relative and absolute basis.

For starters, the Federal Reserve began cutting rates in September of this year, kicking off a long-awaited easing cycle. From our vantage, it seems quite possible that we have entered into a rare non-recessionary rate-cutting cycle that should be supportive of fixed income performance. It is true that Fed Chairman Jerome Powell’s comments at the most recent FOMC meeting disappointed markets by stating that the Fed may act less aggressively than many had hoped. Nevertheless, we remain undeterred. Even after the Fed’s alleged “hawkish comments,” Fed Funds futures are pricing additional rate cuts in 2025. Current monetary policy, the economic backdrop, and relatively attractive starting yields all seems to set up a favorably for fixed income, in our view.

Thus, we believe there is an opportunity for investors who are still parked with overweight balances in money market accounts. Our research suggests that longer-duration fixed income outperforms money markets as rates decline, so we would caution against an excessive overweight in money market funds. Money market funds constantly repurchase securities since they mature within days or weeks of issuance in most cases. This requirement to reinvest proceeds is called “reinvestment risk” and is inherent in all short-term instruments. Longer-term bonds, in contrast, do not face immediate reinvestment risk because they mature over the course of the many years and their prices can appreciate with falling rates.

Stay Active

We favor an active fixed income approach in large part based on the diversity and complexity of the fixed income universe. There are so many different types of securities, and the market does not always price them efficiently, in our opinion. We think that fundamental research can identify pockets of opportunity, while also avoiding areas that are less appealing but still included in many passive fixed income indexes.

Active management might also be able to better navigate the dynamic economic backdrop and uncertain outlook for corporate profits. An easing regulatory environment, the possibility of more corporate M&A activity (i.e., more leverage and debt), and the uncertain impact of new tariffs all require careful monitoring. Thus, we think it behooves investors to be selective and adopt a more defensive posture regarding credit risk. That’s what we plan on doing in our active portfolios.

Meanwhile, two areas that we believe investors should investigate to add incremental yield are through allocations to mortgage-backed securities (MBS) and asset-backed securities (ABS). We project both of these sectors to outperform in 2025. Our analysis of the supply/demand picture for 2025 suggests further MBS spread tightening, while some of the features of ABS may make them a good defensive play, in our view.

As always, uncertainties abound when we enter a new era, and no investment is ever without risk. But through our lens, fixed Income should remain an invaluable part of any diversified investment portfolio given its potential to offset equity risk. This could prove especially valuable given current equity valuations after the run that they have had over the past several years.