Fixed Income: Seeking clarity in muddy waters

Allyson Krautheim 02-Jan-2026

Fixed income investors can hardly be faulted for being a little confused and lacking conviction. After all, 2025 was marked by bouts of volatility stemming from both economic and policy uncertainties. For investors, the outlook has been clear as mud.

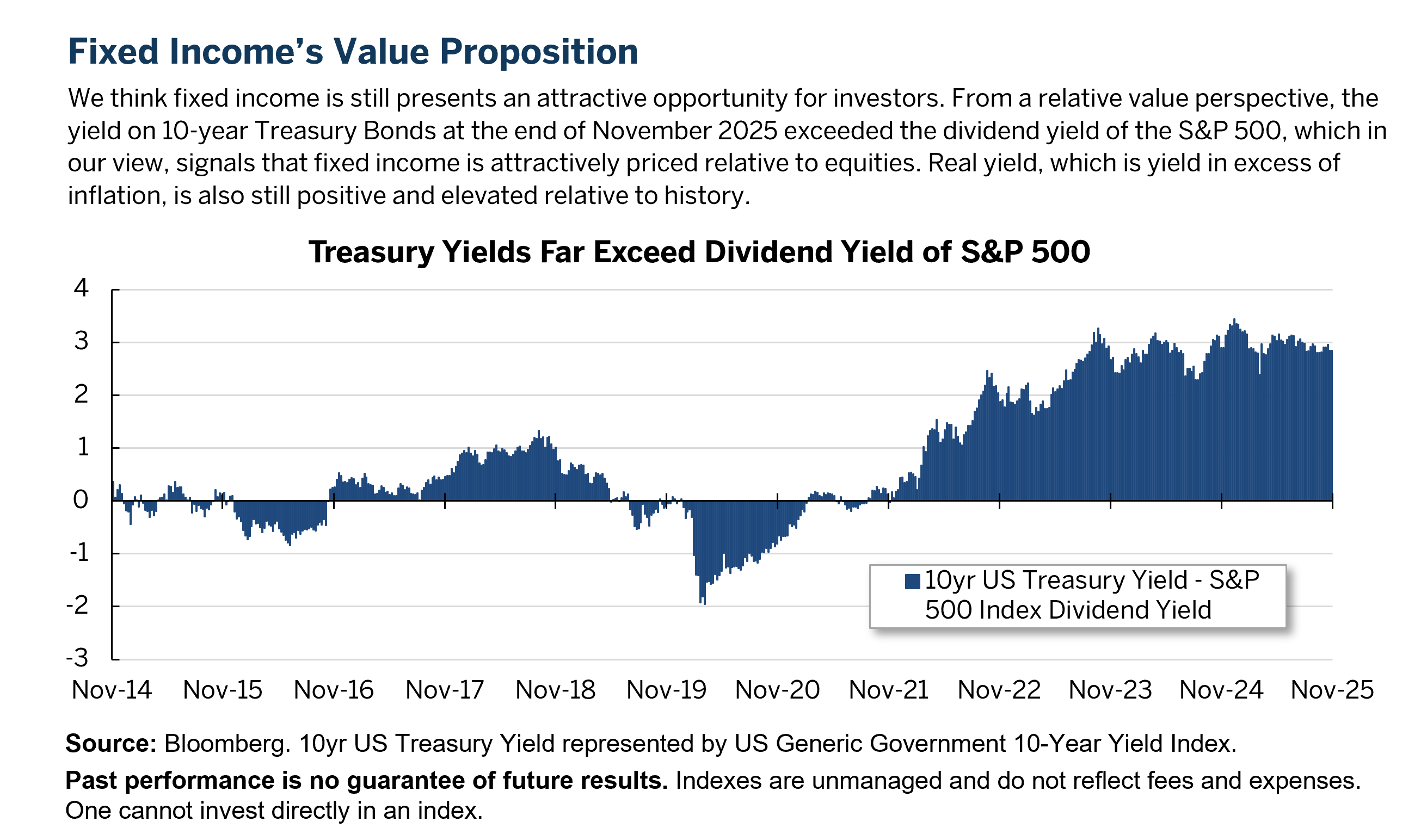

We are always sifting through the macro data and confusing backdrop to help you make sense of all the contradictions. With that in mind, we still believe that fixed income can play an important role for investors, not only for its income generating potential in this environment, but also as a ballast for richly valued equities and other segments of a diversified investment portfolio.

A World of Contradictions

Monetary policy is typically a key driver of yields, so it’s no surprise that during much of 2025 all eyes were focused on the Federal Reserve. While economic data signaled a weaker labor market and inflation remained stubbornly above the Fed’s 2% comfort zone, risk assets (i.e., major equities indexes) continued rallying in the second half and printed new all-time highs in the fourth quarter. So, on one hand stock prices reflected positive investor sentiment, while on the other hand the economy seemed poised to decelerate. If that wasn’t confusing enough, we’ve also had vacillating tariff policies and their uncertain impact on inflation.

Ultimately, the Fed began to cautiously ease rates in September (and tacking on quarter-point rate cuts again in October and December), but future moves look to be data-dependent as the Fed likes to say. Adding to the uncertain near-term direction of monetary policy is the fact that there has been a divergence within the FOMC on which part of the Fed’s dual mandate should be more prominent in setting policy. Should the Fed remain vigilant in fighting inflation and keep rates steady, or should they ease financial conditions to support a weakening labor market? We should also note that Chairman Powell’s term is ending soon, and there will be new leadership and other possible changes in Fed Governors. All this could skew the policy toward being more accommodative. But there is no guarantee—no absolute clarity.

AI & Credit Spreads

Just as artificial intelligence (AI) was a major driver for equities this past year, it also has had an enormous impact on fixed income markets. Debt issuance for AI was nothing short of robust, and if it continues to grow as anticipated in the near term, we would expect to see declining relative value from this segment of the market. In other words, credit may be cheap for the AI borrower, but the growing new debt supply is likely to put upward pressure on credit spreads in 2026. Credit spreads are the incremental yield investors receive for taking on additional credit risk relative to similar duration Treasuries. Wider spreads suggest investors want more compensation to take on the added risk, and all the debt financing for the AI build-out may be shifting risk perceptions across corporate credit markets.

Relative Value?

All these issues might shape how investors want to structure fixed income portfolios in 2026. Certainly nobody can predict how the AI trend will impact the employment picture or whether the Fed will definitively cut rates at the next meeting. However, we still see monetary policy in an overall easing cycle, and our experience suggests that intermediate term core bonds tend to perform well in this environment.

In addition, real yields—loosely defined as a measure of a bond's true return after accounting for inflation—are near the highest they have been in 15 years. Meanwhile, we see investment grade credit spreads at very tight levels, which we think indicates a low probability of generating excess returns by taking on more credit risk. In other words, you might want carefully consider if it’s worthwhile stretching for a tiny bit of incremental yield in lower-rated bonds.

Overall, we remain defensively positioned within the structure of our mandates, but we see value in specific sectors like Treasuries, Agency Mortgage-Backed Securities and Asset-Backed Securities. And perhaps most importantly, we see a fixed income as a steadfast asset class for investors looking for real yield and attractive relative value.