Fixed Income: Keeping pace with rates

JAMES TRACY 07-Jul-2022

Investors are coming to grips with the reality of our new tighter monetary policy. The Federal Reserve is concerned about inflation, and it has been busy ratcheting up interest rates and draining liquidity from the system. While some investors worry about both declining bond prices and their ability to generate enough income to combat inflation, we see the bank loan asset class offering a possible respite. In fact, the variable (i.e. floating rate) nature of this fixed income asset class may offer investors a chance to not only maintain the face value of their fixed income portfolios, but also to capture higher income throughout this rising-rate cycle.

As rates rise, the perceived advantage of the bank loan asset class is largely a function of its structure. The interest rate on floating rate loans generally resets every 90 days based on the three-month London Interbank Offered Rate (LIBOR), which is a short-term interest rate benchmark that major global banks use when lending to one another. Historically, three-month LIBOR follows the ebb and flow of the federal funds interest rate, which is what the Federal Reserve actually controls when implementing its monetary policy.

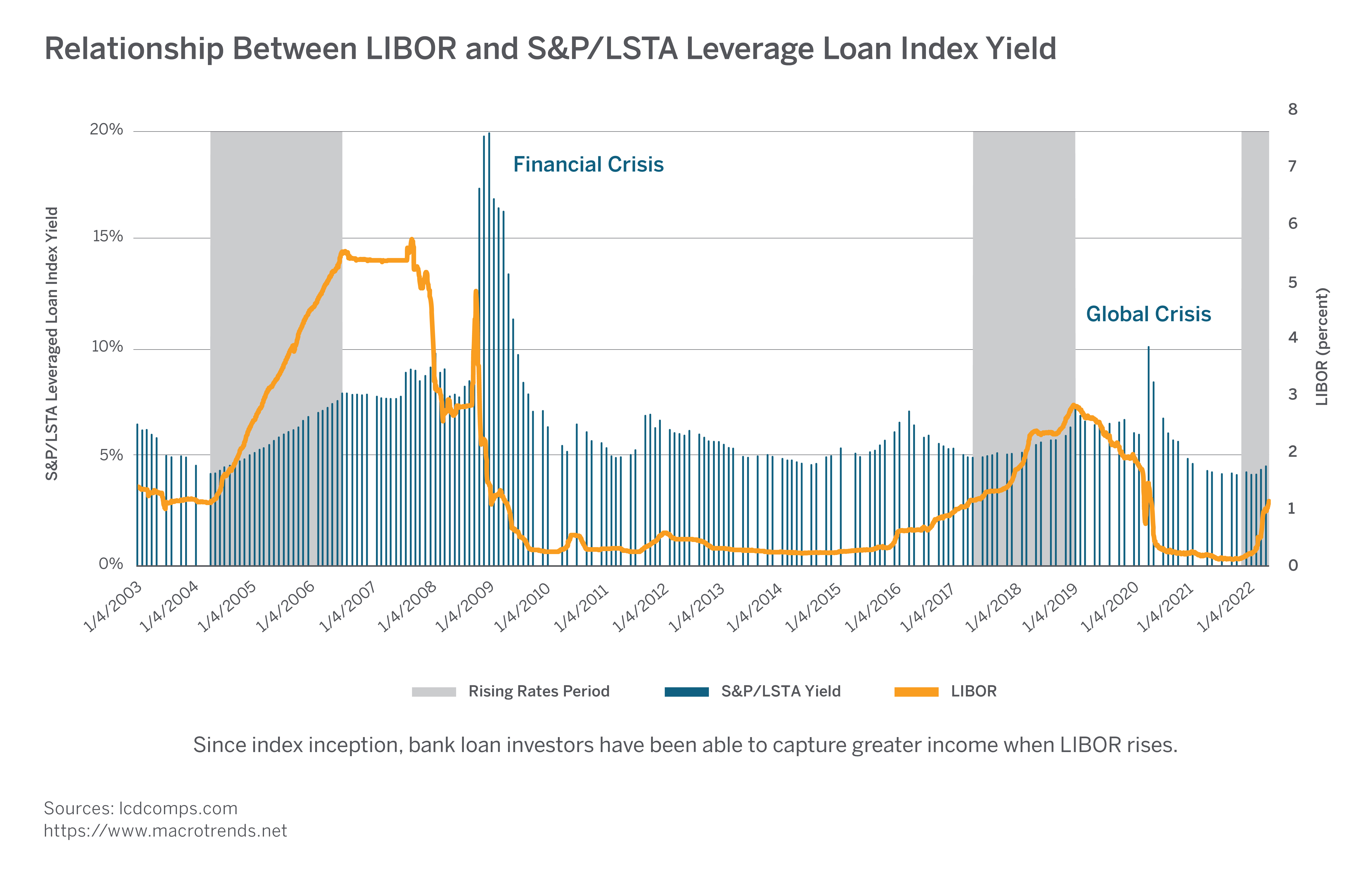

Where do we stand now and where might we be heading? As of mid-June, the fed funds target had climbed to a range of 1.50 to 1.75%, three-month LIBOR was 2.00%, and the yield on the benchmark for the bank loan asset class (using the S&P/LSTA Leveraged Loan Index) was 5.9%. As the graph below illustrates, we also can confirm that the bank loan yield has tended to follow LIBOR, plus a healthy spread of several hundred basis points (with a few exceptions along the way). Looking ahead, the market now expects the fed funds rate to climb to a range of 3.5 to 4.0% by the end of 2023, according to mid-June fed funds futures. Adding on the typical spread can give bank loan investors a general idea of what they might expect in terms of future income, even though we all know that there are no guarantees.

The graph does show two outlier events to the long-term trend—the global financial crisis of 2008-2009, and the beginning of the pandemic in 2019. At both of these times investors eschewed risk assets (both equities and below investment-grade bonds, including bank loans). The yield spike seen in these periods is more a reflection of declining asset prices above all else. After all, yield is simply calculated as the interest paid divided by the price of the underlying bond. Thus, if the face value of a bond falls sharply, yield spikes. This is also called the denominator effect, and it explains the outliers above. Nevertheless, since inception of the bank loan index, the long-term trend data shows how bank loan investors have been able to successfully capture greater income as LIBOR has increased.

A word about risk

It is also true that bank loans carry higher credit risk because they are rated as below investment grade. This asset class is perceived as riskier, and it can fall out of favor with investors in risk-off periods. As we pointed out above, this is what happened during the pandemic and global financial crisis. However, we see relatively strong fundamentals and healthy balance sheets among many corporations. As such, we believe that any such credit risk can be prudently managed by careful security selection. Plus, default rates for leveraged loans remain near historic lows.*

We all know that generating income and trying to keep pace with inflation is a significant issue for many investors. It’s not easy to balance the risks and navigate the headwinds of tighter monetary policy. However, the bank loan asset class might be a candidate for investors who are taking a long look at restructuring their fixed income portfolios in today’s challenging environment.

*Approximately 0.18%, per lcdcomps.com, as of 4/30/2022.