Fixed Income: BBBs punch above their weight class

Allyson Krautheim 12-Jun-2025

When economic uncertainty and volatility threaten to spoil the party, investors tend to pay more attention to their portfolio holdings. This is especially true in fixed income, which is often used to seek to offset equity risk across a broader investment portfolio. With that in mind, some investors have been asking about BBB-rated debt and whether it belongs in a core or core-plus fixed income strategy. In our opinion, the answer is Yes!

Still Investment Grade

A good place to start the conversation might be to reiterate that BBB-rated securities (sometimes listed as Baa3 in Moody's credit rating scale) are still considered investment grade, as opposed to high-yield or “junk” bonds as they are known in the colloquial. BBB bonds are at the lowest rung on the investment-grade ladder, so it’s logical that they may carry more risk compared to bonds with higher ratings. Investors who have historically focused their fixed income investments on A-rated securities may be apprehensive when it comes to investing in this segment of the market. But eschewing BBBs entirely might also mean skipping out on a compelling opportunity set given it’s the largest segment of the investment grade market.

Importantly, the depth and composition of the BBB market has evolved considerably over the years. According to our research estimates, approximately half of the U.S. corporate investment grade world is comprised of corporate issuers rated in the BBB+ to BBB- range. We have seen many high-quality companies make conscious decisions to transition from an A credit rating to BBB rating as they have recognized the consistent depth, liquidity and capital available for corporate issuers in that ratings band. For example, current BBB issuers include widely known companies, such as Boeing, McDonalds, Verizon, CVS and General Mills, among others. These household names might surprise some investors. Moreover, while the higher A-rated segment of the market is heavily weighted towards banks, the BBB market segment actually provides a diverse opportunity set across many industries.

Low Historical Default Rates

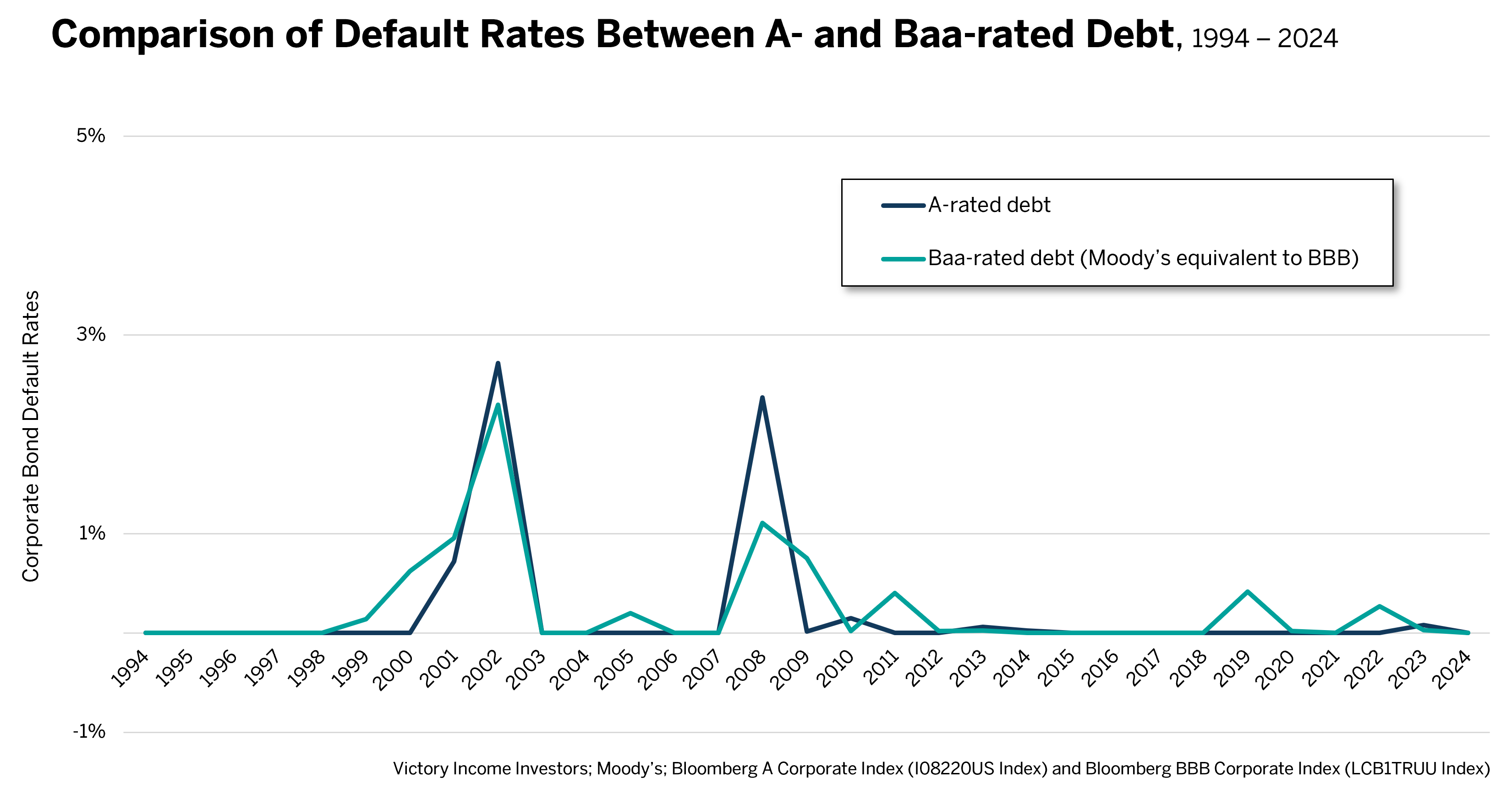

As always, investors are right to demand a higher potential reward (i.e., yield) for assuming more risk, whether that’s credit risk, duration risk, or any other form of risk inherent to fixed income. However, defaults in the BBB market segment are not as commonplace as some investors may believe. Digging into the historical data, our research suggests default risk—the likelihood that a bond issuer will not make interest payments on schedule or otherwise fail to repay the principal in full—has not been severe. To the contrary, we think that investors in BBB securities are being well-compensated to take on the higher credit risk. Going back three decades, Moody’s Investor Service default data for global corporate bond issuers reveals similar annual default rates for both Baa (Moody’s equivalent of BBB rating) and A-rated issuers, for the period 1994-2024. In some years, the annual default rates for the BBB segment have even been less than those for the higher A-rated market segment. The graph below illustrates the point.

A Yield Advantage

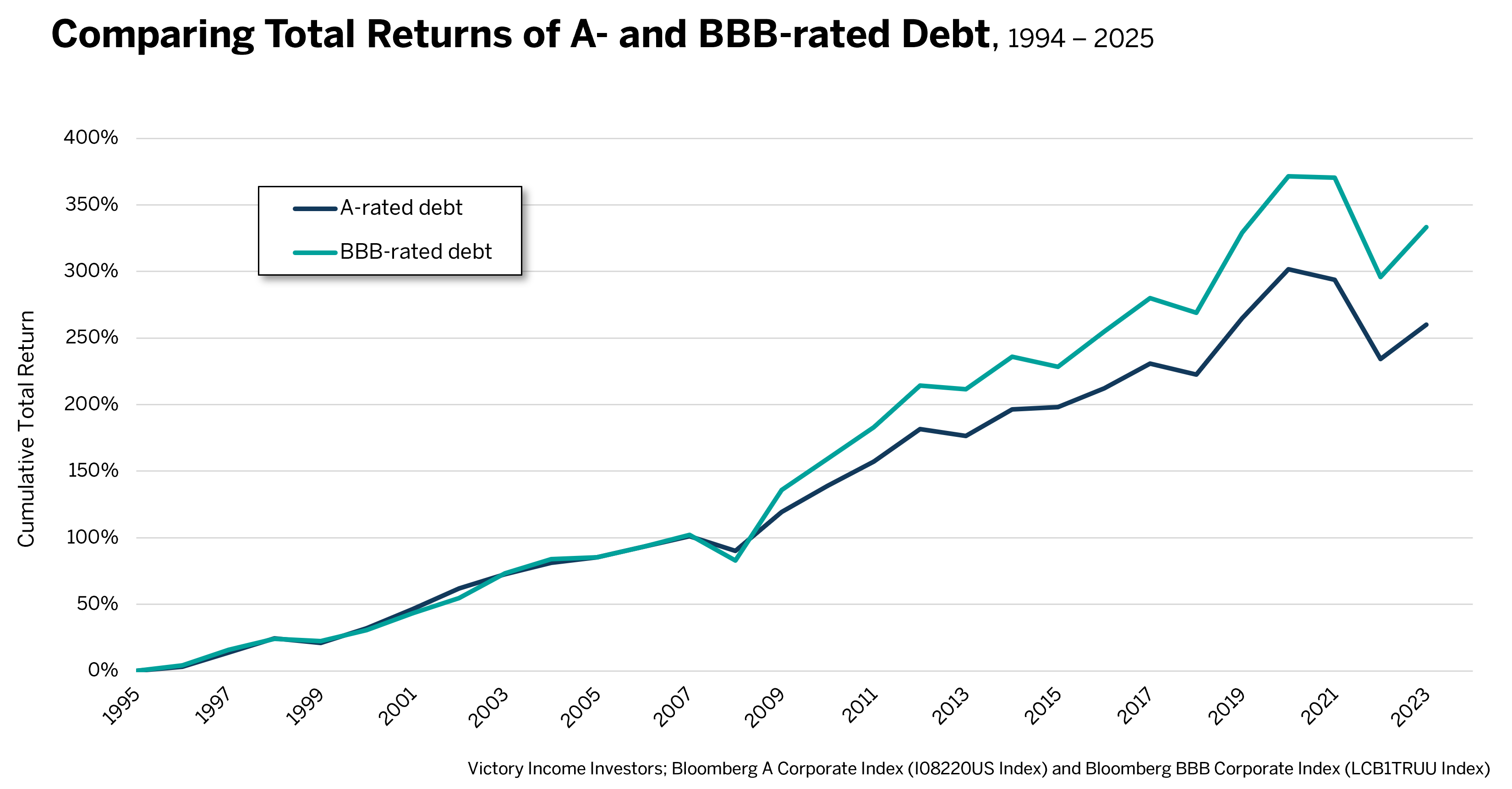

Ultimately, the attractiveness of the BBB market for most investors has been validated by the investment return over the years. The graph below shows the total returns—yield plus price appreciation—for the BBB-rated versus A-rated bonds in the U.S. corporate investment grade market.

Of course, we all know that past performance is no guarantee of future results. And we also know that there is no free lunch in investing, so to speak. The promise of higher yield comes with higher risk. Yet within this BBB segment of the debt market, we see ample opportunities, particularly for active managers. An active manager should be adept at digging into the balance sheet of an issuer, understanding industry trends and the specific advantages/disadvantages of each issuer among its peer group. Importantly, an active manager who does independent credit research—as opposed to relying exclusively on the mainstream ratings agencies—can be an advantage in uncovering hidden value.

In building portfolios of BBB securities, we also believe that maintaining diversification across industries and geographies is essential to help manage any added credit risk. And we think that having the size and scale to access new issuance is also critical. That’s not something that every active fixed income manager offers.

In the end, we have studied the market and believe that BBB bonds have the potential to deliver a yield boost for portfolios in a risk-appropriate manner. We urge investors not to discount the power of BBB-credits based on preconceived and sometimes incorrect notions of high default risk. Through our lens, and using our proven investment research risk management protocols, we think BBB securities can punch above their weight, even in today’s uncertain environment.