Financial Markets: The low-vol phenomenon

Scott Kefer, CFA 18-Aug-2022

It’s been a tumultuous year for equity investors. The first two quarters were some of the most challenging in decades, only to be followed by a snap-back in summer. In this volatile environment, it’s worth reminding investors that they may not need to take on the most risk to achieve better longer-term returns.

The low-vol anomaly

One of the enduring myths held by investors is that buying higher-risk equities equates to higher returns. Not so fast! The low-vol phenomenon (or the low-vol anomaly) suggests that investors may be able to achieve better long-term results not by taking on greater risk, but rather by avoiding the steepest drawdowns that often accompany the riskiest assets. The root causes for this seeming anomaly are many and include aspects from behavioral economics. After all, investors love to boast about finding that epic stock with “eye-popping” returns, which might occasionally happen but often comes with excessive risk and dramatic pullbacks.

Many fast-growing businesses and other story-stocks do boast disruptive business models or intriguing products. Although they may be growing quickly and have exciting return potential, they often are not profitable today. The high risks associated with these types of stocks also means that if the story shifts or the momentum turns, any gains can be quickly erased. For example, some stocks offer binary outcomes—such as a biotech focused on a singular drug that will either be granted approval…or not. This is not to say biotechs or other types of risk assets don’t have a place in a diversified portfolio. Rather, what the low-vol phenomenon suggests is that structuring an equities allocation and skewing it toward lower-volatility stocks might make more sense for the long haul. Slow and steady can win the race.

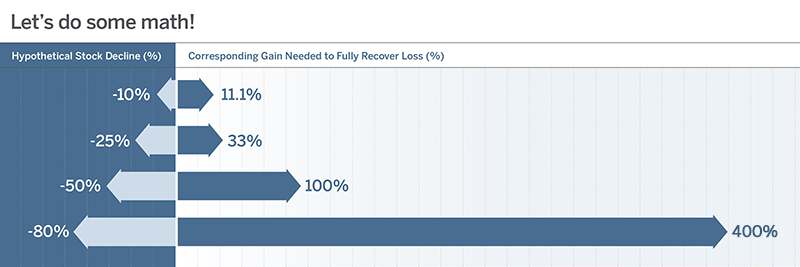

The ultimate reason to consider lower-volatility strategies as part of a core equities allocation is rooted in math. Investors must recognize that gains and losses in a portfolio are not equally proportional. In other words, the more a stock declines, the more it needs to go up to get back to even. Consider the chart below:

A few periods of sharp losses can more than offset the hard-fought gains achieved over time. Thus, in order to outperform through all stages of a market cycle, it is more important to avoid the punishing effects of steep drawdowns rather than hit the occasional home run.

Of course, it’s also important to remember that low-vol strategies are likely to underperform during times of risk-on when momentum factors and other high-growth characteristics are being rewarded by investors (sometimes exuberant investors). But in times of tumult, these low-vol strategies aim to minimize steep drawdowns, and in doing so they offer the potential to compound returns at a higher rate over a long period. That’s how the math works, and it’s something often overlooked by investors in rabid bull markets.

Dig into the details

Before allocating, investors may want to take a hard look at how these low-vol strategies are constructed and whether they expose investors to some potential unintended consequences. The simplest (and among the most popular) low-vol approach is to buy a basket of stocks with the lowest trailing 12-month volatility. Yet such a narrowly focused approach sacrifices diversification on a portfolio level and is likely to include slow-moving equities with poor fundamentals. Often this means a portfolio concentrated in Utilities or Consumer Staples. This might fulfill the low-volatility objective, but such an approach seems a blunt way to achieve a goal that is unlikely to offer good results across all market environments.

In contrast, we think a better approach is minimum-volatility strategy that also allows for the layering of different constraints, such as sector limitations to ensure better diversification. That may be a clear improvement versus tracking a rudimentary low-vol index. But taking it one step further and adding in some fundamental analysis might offer yet another enhancement to this concept. For example, screening for an array of Quality, Value or other investment factors* in conjunction with lower-volatility could result in a portfolio of higher-quality companies with less downside capture potential.

This type of innovative minimum volatility approach might prove to be a valuable addition to a core equities allocation—one that’s not tied to the vagaries of the few stocks that tend to drive performance in the S&P 500® Index. Importantly, this approach should be less exposed to violent equity drawdowns (although obviously not immune from pullbacks). In the end, a smoother return profile could help investors sleep better at night while also offering a path to better long-term returns thanks to the low-vol phenomenon.

*Investment factors, such as Value, Momentum, Quality, Minimum Volatility, Size are used to target specific drivers of returns