The Roth IRA has, since 1998, been a popular retirement savings vehicle. It is the second most frequently owned type of Individual Retirement Account. Nearly 25 million Americans own a Roth IRA.1 It may well play an important role in retirement planning. But its features and benefits may make it a practical vehicle to achieve other financial planning objectives. When used creatively, the Roth IRA transcends its intended purpose as a retirement savings account.

What are the features and benefits of the Roth IRA?

The most recognized feature of Roth (and Traditional) IRAs is their tax deferral. Investment returns on funds held in these account are not taxed. But Roth IRAs have an additional tax advantage. Typically funds withdrawn from a Roth IRA aren’t taxed. The reason for this is that the contributions you make come from after-tax dollars.

Still, withdrawals are subject to a couple of rules. To be “Qualified Distributions” that avoid an early withdrawal penalty, funds must remain in your Roth IRA for five years. You must also be age 59½ or older before you take money out.

You can access funds in a Roth IRA before that. But they’ll typically be subject to a 10% early withdrawal penalty. There are exceptions for hardships and special circumstances. But the intent of the account is to sock money away for a long time. This is an important feature in helping you maximize the account’s benefits.

Using Your Roth IRA Before Retirement

Your Roth IRA may provide financial planning opportunities beyond saving for retirement. Investors with well-funded retirement accounts, like a 401(k) or the Thrift Savings Plan (TSP) and those with predictable retirement income coming from a defined benefit plan, may be able to use their Roth IRAs to finance other high priority consumption goals.

Investors use many types of savings vehicles to finance their non-retirement objectives, including:

- Money market accounts

- Passbook savings accounts

- Certificates of deposit

- Taxable brokerage accounts

Consumption goals that extend beyond a few years may also be financed using mutual funds, ETFs, or other securities with long investment horizons.

Because a Roth IRA is funded with after-tax dollars it may be used to finance many consumption goals. For example, emergency funds, vacation funds, or a home down payment fund.

So, matching the time horizon of individual investments with the time frame of specific savings objectives may be an appropriate strategy. And a Roth IRA may be an appropriate vehicle to finance them.

There are a number of reasons for this. Like many other savings accounts, a Roth IRA is funded with after-tax dollars. The Roth also offers tax benefits others don’t. Returns in a Roth IRA can compound unconstrained by taxes. Qualified distributions are not taxable. So, a Roth IRA is typically a more tax efficient savings vehicle.

If funds are required in an emergency before you reach age 59½, there may be an exception available to avoid the early withdrawal penalty. That is certainly the case if you withdraw money to buy or build a first house.

Investments in a Roth IRA can be tailored to match both the time horizon of the objective and your specific risk tolerance.

Using Your Roth IRA Opportunistically

A Roth IRA can be a creative component of your overall retirement plan. Two particular techniques help illustrate this.

1) Roll an employer-sponsored retirement account into a Roth IRA

2) Convert an existing Traditional IRA into a Roth

These two moves typically create taxable income. But in some cases paying the tax may make sense over the long term. This may be the case when you expect your tax rates to be higher in the future than they are now.

A good example of the opportunity to roll an employer-sponsored retirement account into a Roth IRA is when you separate from military service. Servicemembers often leverage their military experience into higher-paying civilian employment. This may put them in a higher tax bracket.

TSP assets rolled into a Roth IRA will be subject to income tax at your current rate. But they will be allowed to grow tax free after that. When you reach age 59½ the qualified distributions you take from that Roth IRA will also be completely tax free, regardless of how much the funds have grown over time.

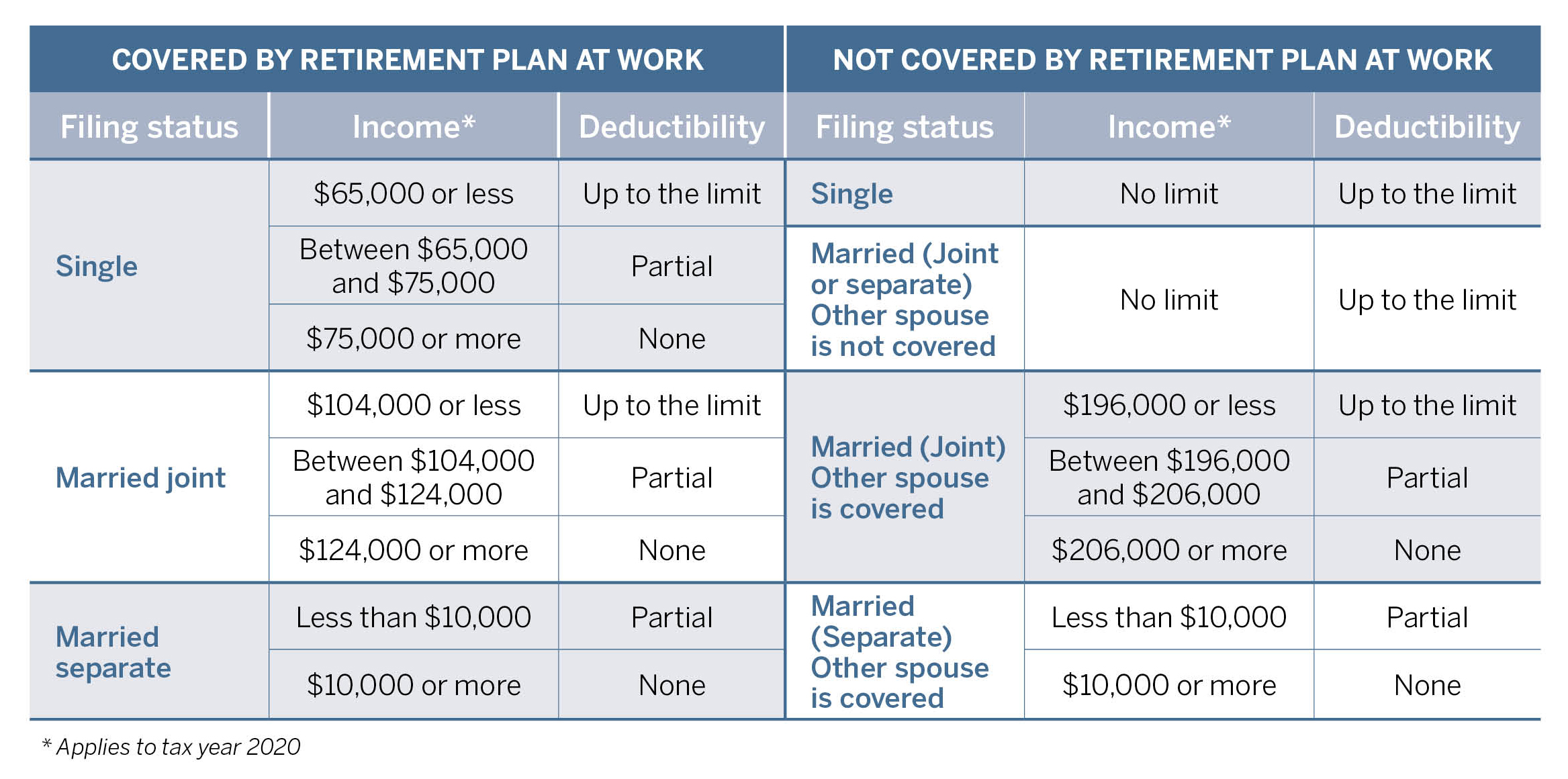

Converting a Traditional IRA into a Roth IRA creates an interesting opportunity for high-income taxpayers. Above certain income limits (see table below), you cannot contribute to a Roth IRA.